AI Wealth Strategy

A graduate strategy project — for Fordham's AI for Strategic Decision Making course — advising a community bank's board on deploying a RAG-grounded AI wealth assistant across Azure, backed by a quantified financial case and a standing algorithmic-bias audit protocol.

For Fordham's AI for Strategic Decision Making course, my team — which we named "Alpaca Consulting Partners" — advised the board of a case-study community bank on whether and how to deploy an AI wealth assistant. The deliverable was a full strategy package: a white paper, an Azure architecture, an 18-month roadmap, and an executive presentation — grounded in a quantified financial case and a governance protocol.

As Technical Implementation Lead I owned the technical case behind the recommendation — the RAG grounding, the risk model, and the Monte Carlo ROI simulation. The hard part wasn't the model; it was turning it into something a board could defensibly act on.

A community bank wanted to modernize its wealth advisory offering with AI, but faced the questions every regulated institution asks first: Is it compliant? Is it worth it? Will it treat clients fairly?

- The user — a bank board deciding on a material technology investment under fiduciary and regulatory constraints.

- Why it matters — hallucination and bias aren't UX bugs here; they're compliance and legal risk.

- The bar — a recommendation had to be quantified, stress-tested, and governed, not just plausible.

- Grounded assistant — grounded in the bank's own policy documents via Azure AI Search + Azure OpenAI GPT-4, with retrieval-cited responses to prevent hallucination and support fiduciary compliance.

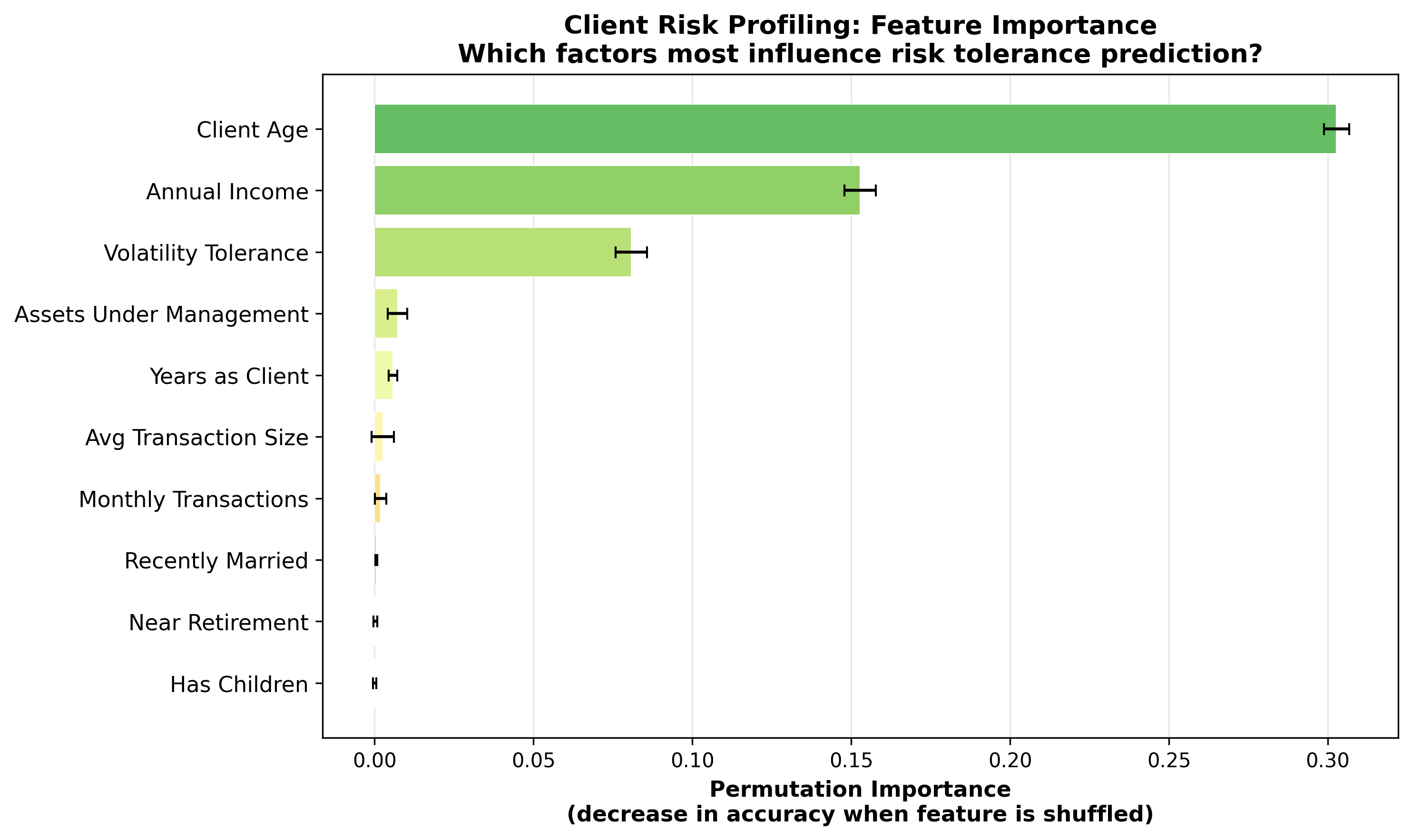

- Risk profiler — a Gradient Boosting model trained on 25,000 synthetic clients calibrated to census demographics, reaching 77% cross-validated accuracy predicting risk tolerance across four categories.

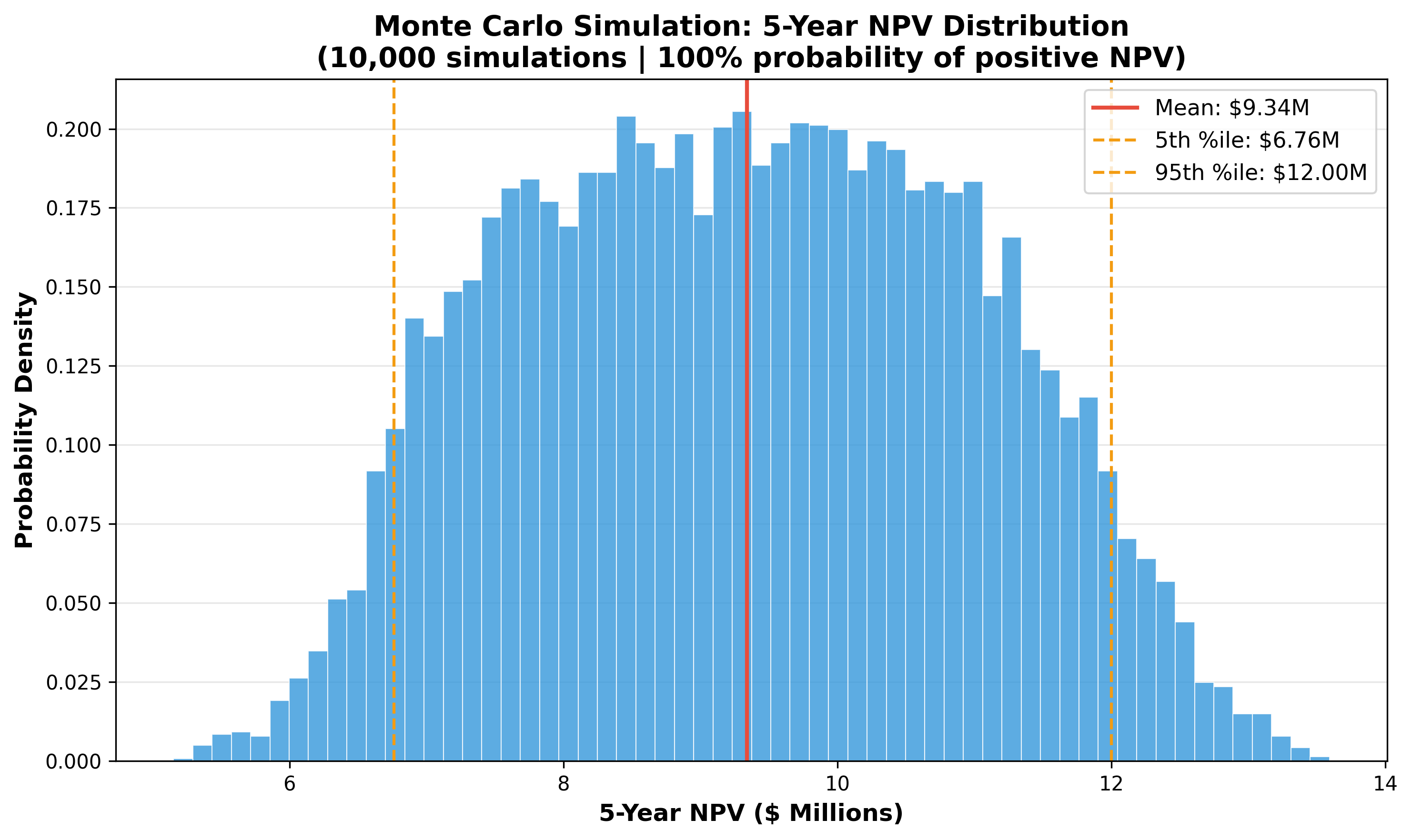

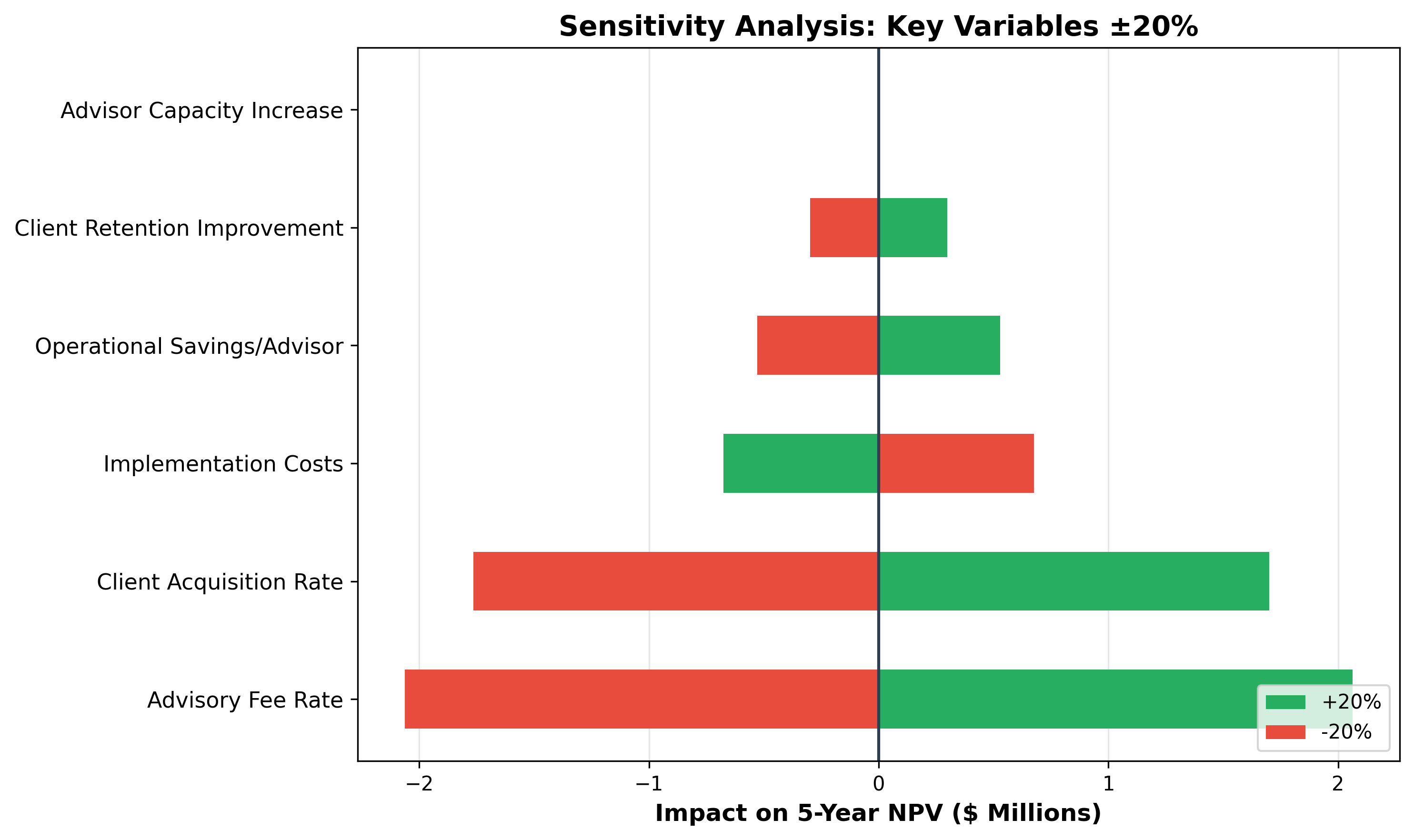

- Quantified case — a Monte Carlo ROI model across 10,000 scenarios projecting $9.6M NPV, 87% IRR, and Year-1 break-even, with sensitivity/tornado analysis identifying advisory fee rate and client acquisition rate — not implementation cost — as the dominant drivers.

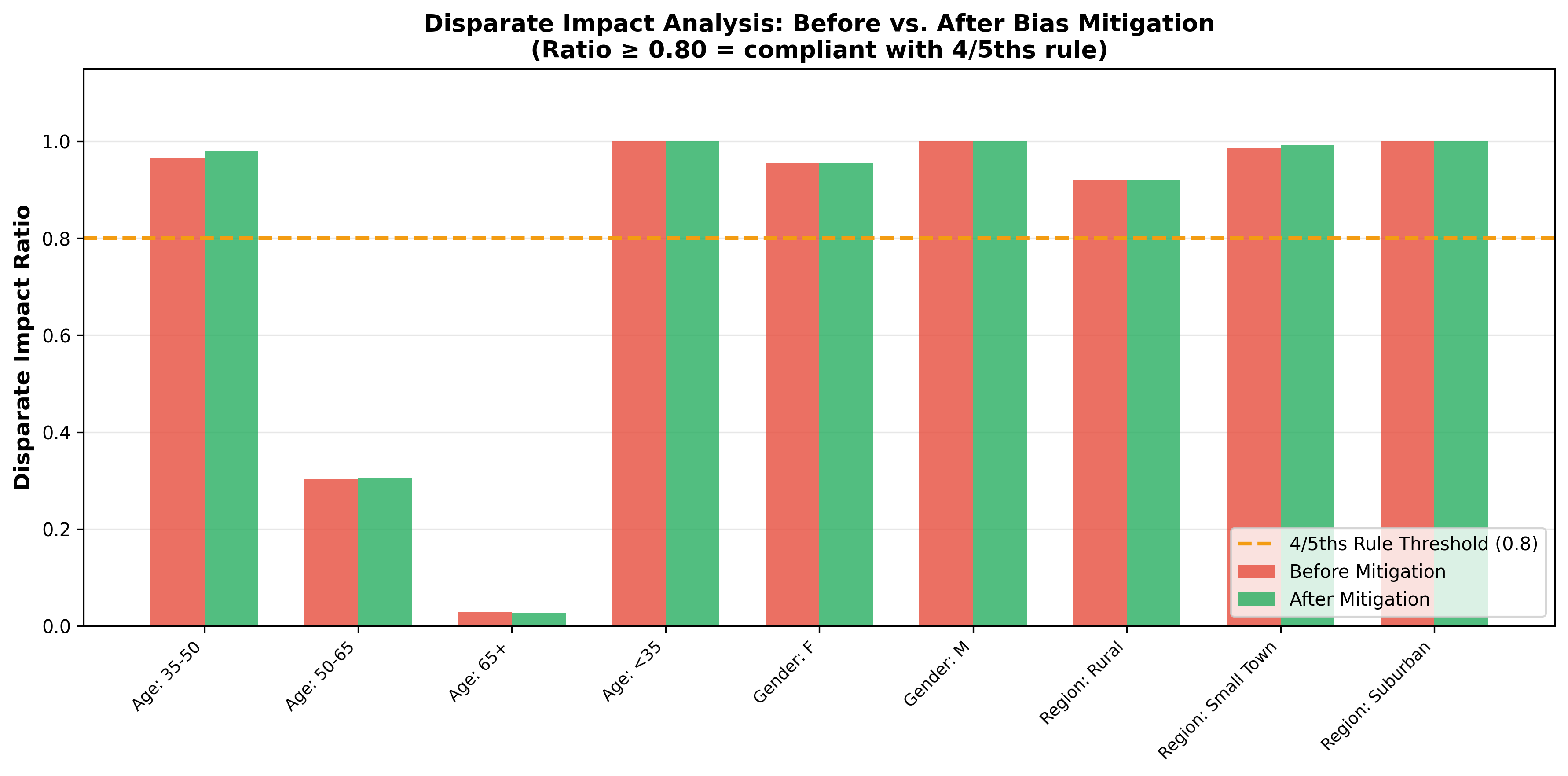

- Bias governance — a quarterly algorithmic-bias audit using the EEOC 4/5ths rule; any group below a 0.80 disparate-impact ratio triggers mandatory human review, with mitigation via re-weighting at under 0.3% accuracy impact.

- Proving value under uncertainty. A single ROI number is easy to dismiss. Ten thousand Monte Carlo scenarios with a worst-case 5th-percentile floor of $6.8M NPV made the case credible to a skeptical board.

- Fairness as a hard requirement. Encoding the EEOC 4/5ths rule into a recurring audit turned "we care about bias" into an enforceable control with a defined trigger.

- Compliance-first grounding. Retrieval-cited responses over the bank's own policies were non-negotiable for fiduciary defensibility.

- For a regulated buyer, governance and a stress-tested financial case are the product — the model is table stakes.

- Sensitivity analysis reframed the conversation: the board cared far more about fee and acquisition rates than implementation cost, which changed the recommendation.

- Next: a live pilot to replace synthetic-client calibration with real data, and continuous bias monitoring rather than quarterly batches.